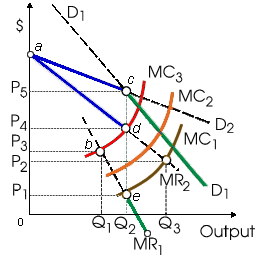

Into this "kinked-demand" model, such firm views the marginal revenue curve this faces as the: (1) linear curve acD2 for all prices. (2) linear curve deMR1 for all prices. (3) nonlinear curve adeMR1. (4) linear marginal revenue curve adMR2.

Hello guys I want your advice. Please recommend some views for above Economics problems.