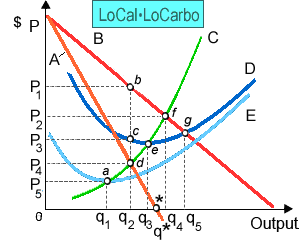

LoCalLoCarbo has turn into the favorite of fad dieters. There in demonstrated figure curve A shows: (i) LoCalLoCarbo’s marginal cost curve. (ii) LoCalLoCarbo’s average variable cost curve. (iii) LoCalLoCarbo’s average total cost curve. (iv) the market demand curve facing LoCalLoCarbo. (v) LoCalLoCarbo’s marginal revenue curve.

How can I solve my Economics problem? Please suggest me the correct answer.