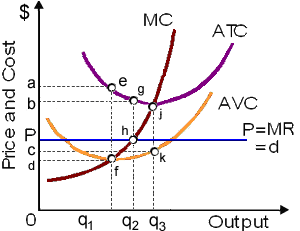

Hey friends I need your suggestion for this query about the profit and losses as illustrated graph when this firm produces q2 output, in that case its: (w) MR > MC. (x) MR < MC. (y) MR = MC. (z) P > MC.

Please give me right answer for the same.

Can someone explain/help me with best solution about problem of Economics...