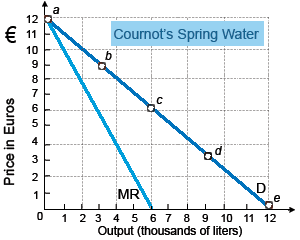

Monsieur Cournot has a monopoly on an artesian well from that flows tasty spring water along with medicinal properties. To ignore variable costs, he insists which customers bring their own pails as well as fill them individually. Cournot’s business policies give in marginal costs for producing and selling artesian spring water which equal: (1) €8 per liter. (2) €6 per liter. (3) €4 per liter. (4) €2 per liter. (5) zero.

Hello guys I want your advice. Please recommend some views for above Economics problems.