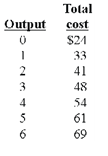

Marginal cost

Give the answer of following question. Refer to the given data. The marginal cost of producing the sixth unit of output is: A) $24. B) $12. C) $16. D) $8.

Economists generally suppose that the firms behave rationally to make the most of: (1) Employment. (2) The community’s economic welfare. (3) Workers’ satisfaction. (4) Gains. Can someone please help me in finding out th

Congratulations! You have made a fortune after establishing the firm which publishes bestselling books of the economic poetry. Your implicit costs comprise: (1) Salaries for your firm’s website designer. (2) The value of your time. (3) Fees for cleaning the serv

When a 10% hike in the price of paisley socks causes sales to fall with 20%, the demand for such socks is: (1) perfectly inelastic. (2) relatively inelastic. (3) unitarily elastic. (4) relatively elastic. (5) perfectly elastic. <

“Law of Distribution” given by Vilfredo Pareto asserts that the: (w) relative prices for goods reflect how intensively labor is used as an input. (x) the percentages of national income going to labor and to capital is a co

When this firm is typical in illustrated figure of this purely competitive market and when this is a constant-cost industry, in that case the long run supply curve for the industry is a horizontal line which would go from: (1) point c

I have a problem in economics on Law of Demand in respect to relative price. Please help me in the following question. The law of demand defines that as: (1) Absolute prices rise, quantity demanded raises. (2) Relative prices raise, quantity demanded

For a negative income tax the break-even level of income plan (NIT) is: (1) negatively related to the plan’s basic income floor. (2) positively related to the negative income tax rate. (3) a main influence on the total cost of t

The percentage change within quantity demanded along this demonstrated linear demand curve is: (w) greater than the percentage change within price in range b. (x) smaller than the percentage change within price in range a. (y) precise

Payments for a resource into excess of the minimum needed to supply specified amounts of the resource are termed as: (1) economic rents. (2) wage premiums. (3) excess profits. (4) surplus values. (5) capitalization. Q : Regulatory barrier to entry Billy Billy recently invented and in that case patented a motorized flying skateboard which transports people to and from their destinations in less than half the time this would take to ride or drive a bus. Billy is protected from competition from a: (1) regulatory barrier

Billy recently invented and in that case patented a motorized flying skateboard which transports people to and from their destinations in less than half the time this would take to ride or drive a bus. Billy is protected from competition from a: (1) regulatory barrier

18,76,764

1934457 Asked

3,689

Active Tutors

1429349

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!