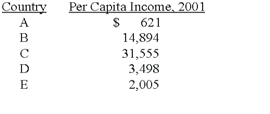

Low-income developing countries

select the right answer of the question. Which of the below nations are low-income developing countries (DVCs), according to the World Bank? 1) country A only 2) countries A, D, and E 3) countries A and E 4) countries A, B, D, and E

When both population and per capita income grow across time, in that case your income will tend to be most erratic but the goods you sell are: (1) both income inelastic and price inelastic within demand. (2) a large part of classical

Economists generally use the word “competition” to refer to: (w) negotiations among buyers and sellers. (x) a type of market structure in that competitors are price takers and, occasionally, to rivalrous processes among firms. (y) how pric

Name the System of Note-issue in India. Answer: In India, the system of note-issue is the Minimum Reserve System. The RBI is needed to keep minimum reserves of Rs 2

Give the answer of following question. Which of the following sayings associate most closely to the idea of sunk costs? 1) Don't cry over spilt milk. 2) A bird in the hand is worth two in the bush. 3) He who hesitates is lost. 4) Show me the money.

In a competitive pricing strategy how does one can arrive for a multi-service practice where there are no specific products in question?

Illustrate and explain using diagrams, the difference between long run supply in a constant cost individual firm and industry and an increasing cost firm and industry.

Negative income elasticities of demand entail those goods are: (1) luxuries. (2) necessities. (3) inferior. (4) substitutes. (5) expensive. Can anybody suggest me the proper explanation for given problem regarding

Contestable markets and purely competitive markets are related in that both: (w) consist of large numbers of firms. (x) consist of firms who are price takers. (y) are characterized by easy entry. (z) are characterized by large economies of scale.

Marginal revenue: This is the change in total revenue by selling one more or a lesser amount of unit of commodity.

When wage discrimination is not probable for the first 40 workers this profit-maximizing organization hires, however it can wage discriminate perfectly whenever hiring all the subsequent workers, it hires a net of: (p) Forty workers at an average salary of $700 per we

18,76,764

1934781 Asked

3,689

Active Tutors

1458838

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!