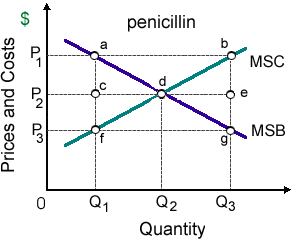

When pharmaceutical manufacturers conspire to generate only Q1 penicillin, in that case the: (i) purely-competitive firms which produced penicillin would experience economic losses. (ii) resulting excessive antibiotic treatments would produce strains of drug-resistant diseases. (iii) marginal social benefits of penicillin would exceed the marginal social costs. (iv) loss in social welfare would approximately equivalent the area of triangle bdg. (v) marginal social costs of penicillin would exceed the marginal social benefits.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.