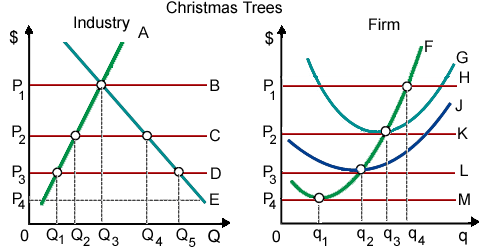

When Christmas tree farming is a decreasing cost industry and this firm is typical, in that case an increase in the market demand for Christmas trees will give in a long run equilibrium price: (1) greater than P1. (2) less than P2. (3) more than P3 but less than P2. (4) more than P4 but more than P3. (5) less than P4.

Hello guys I want your advice. Please recommend some views for above Economics problems.