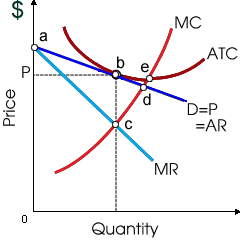

This monopolistic competitor produces Q0 units and is demonstrated: (w) earning total profit equal to 0PbQ. (x) as a price taker. (y) setting price equal to marginal revenue. (z) in long-run equilibrium.

Please guys help to solve this problem of Economics with some explanation.