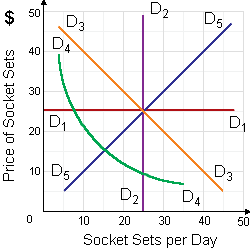

The demand curve for socket sets from the list below which is least consistent along with the law of demand is: (w) demand curve D1D1. (x) demand curve D2D2. (y) demand curve D3D3. (z) demand curve D4D4.

How can I solve my economics problem? Please suggest me the correct answer.