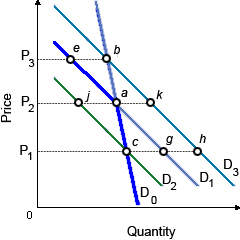

In this kinked demand curve model as in given graph, when this firm operated at point a and lowered its price by P2 to P1 and other firms in the industry also lower prices, in that case this firm will move from point a to: (w) point g. (x) point c. (y) point h. (z) point j.

Please choose the right answer from above...I want your suggestion for the same.