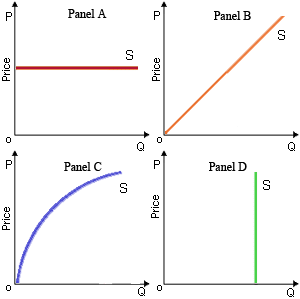

The price elasticity of supply in given grph is infinite therefore supply is perfectly price elastic within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

I need a good answer on the topic of Economic problems. Please give me your suggestion for the same by using above options.