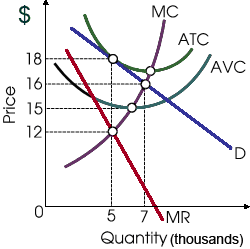

This profit-maximizing firm in illustrated graph will never knowingly generate: (w) where MR is positive. (x) where MR is falling. (y) on the elastic proportion of the demand curve. (z) on the inelastic proportion of the demand curve.

Hello guys I want your advice. Please recommend some views for above Economics problems.