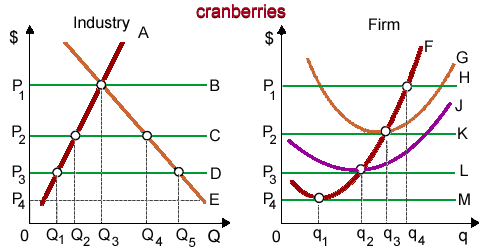

When cranberry farming is an increasing constant cost industry and that firm is typical, in that case an increase within the market demand for cranberries will give in a long run equilibrium price as: (i) less than P1. (ii) greater than P2. (iii) less than P2 but more than P3. (iv) less than P3 but more than P4. (v) less than P4.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?