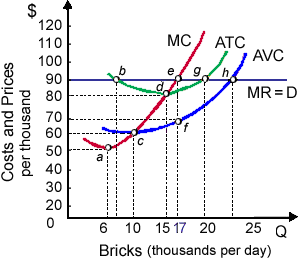

Raised market demand for generic bricks would result within a(n) ___________ into the price of bricks as well as a(n) ___________ within this brickyard’s profit-maximizing output. (i) increase; decrease. (ii) increase; increase. (iii) decrease; decrease. (iv) decrease; increase.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?