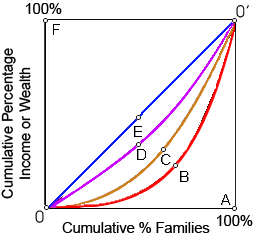

When you were unconcerned about the welfare of other people and your income rated you onto the top two percent of the population, then you would be happiest while the Lorenz curve for your country resembled as: (1) line 0A0'. (2) line 0B0'. (3) line 0C0'. (4) line 0D0'. (5) line 0F0'.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?