Income elasticity of demand

Income elasticity of demand: Income elasticity of demand is the degree of receptiveness of demand to the modification in income.

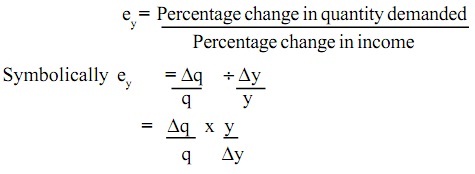

Income elasticity of demand:

Income elasticity of demand is the degree of receptiveness of demand to the modification in income.

When you were in the ski boat business, your net revenues from selling given numbers of boats would be least influenced by: (i) Govt. increasing fees for boat licenses. (ii) Rises in prices for jet skis. (iii) Pay hikes for dock-workers. (iv) Vacation

The best illustration of an oligopoly is: (1) guaranteed next-day delivery of packages and mail. (2) cranberry production. (3) all the local electric utility companies in New England. (4) the United Autoworkers [UAW] union. (5) Wal-Mart.

The consumption and saving schedules demonstrate that: A) consumption rises, but saving declines, as disposable income rises. B) saving varies inversely with the profitability of investment. C) saving varies directly with the level of disposable income. D) saving is i

The purely competitive firm in the output market which hires from a purely competitive labor market will employ the labor at the point where VMP = W as the firm: (i) Operates in society's best interest. (ii) Wants to be quite fair to workers. (iii) Is egalitarian inst

Poverty stricken families are seldom described by: (w) a female headed household. (x) higher labor force participation rates. (y) more frequent illnesses. (z) higher birth rates and more children. Hey friends pleas

Economic losses in an industry generate competitive pressures which cause: (1) industry output to fall. (2) market price to decrease. (3) each firm’s short-run output to increase. (4) rising costs for industry inputs. (5) firms to expand product

Open market operation signifies to the sale and purchase of securities by the Central Bank in case of deficient demand whenever AD falling short of AS at full employment, the Central Bank purchases securities in open market and makes payment to the se

The problem of asymmetric information is that

Choose Which one best describes the invisible-hand concept? 1) The desires of resource suppliers and producers to further their own self-interest will automatically further the public interest. 2) The nonsubstitutability of resources creates a conflict between private

For Cournot’s Spring Water the demand is relatively price inelastic at: (i) point a. (ii) point b. (iii) point c (iv) point d. (v) point e. Discover Q & A Leading Solution Library Avail More Than 1461405 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1954566 Asked 3,689 Active Tutors 1461405 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1954566 Asked

3,689

Active Tutors

1461405

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!