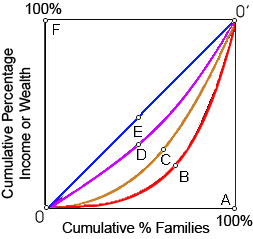

When line 0C0' shows income distribution before taxes and transfers, in that case the line that shows income distribution after taxes and transfers would be: (1) line 0A0'. (2) line 0B0'. (3) line 0C0'. (4) line 0D0'. (5) line 0E0'.

Hey friends please give your opinion for the problem of Economics that is given above.