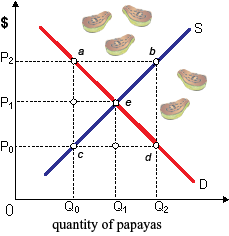

A surplus of papayas would involve when: (1) government set a price ceiling of P1. (2) growers expected prices to soar. (3) hurricanes vanished all Central American papaya plantations. (4) government imposed a price floor of P2. (5) seller's supply prices rise to P1.

Hello guys I want your advice. Please recommend some views for above economics problems.