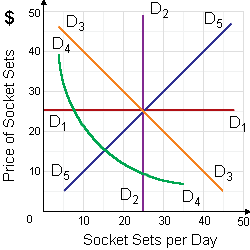

In this figure demonstrating hypothetical demands for socket sets, there demand curve: (1) D1D1 is perfectly price-inelastic. (2) D2D2 is perfectly price elastic. (3) D3D3 has a price elasticity coefficient of one. (4) D4D4 has a price elasticity coefficient of infinity. (5) D1D1 is perfectly price elastic.

Can someone explain/help me with best solution about problem of economic...