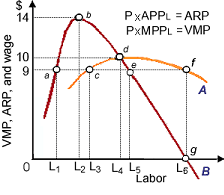

When this purely competitive firm can hire any amount of labor at pre hour wage of $9 per worker, in this given figure, as it will hire: (1) L2 workers. (2) L3 workers. (3) L4 workers. (4) L5 workers. (5) L6 workers.

Please choose the right answer from above...I want your suggestion for the same.