Greatest total revenue at price

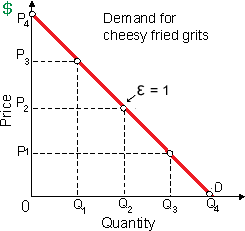

In the demonstrated figure, total revenue is greatest for cheesy fried grits of Pixie at a price of as: (w) P1. (x) P2. (y) P3. (z) P4. Can someone explain/help me with best solution about problem of Economics...

In the demonstrated figure, total revenue is greatest for cheesy fried grits of Pixie at a price of as: (w) P1. (x) P2. (y) P3. (z) P4.

Can someone explain/help me with best solution about problem of Economics...

I have a problem in economics on Consumer goods-Durable and nondurable. Please help me in the following question. Consumer goods comprise durable and nondurable goods, and: (i) Capital equipment. (ii) House-hold goods. (iii) Services. (iv) Electronic goods.

Can someone help me in finding out the right answer from the given options. Whenever the quantity of a good supplied surpasses the quantity demanded: (i) Unexpected growth of inventories will cause prices to drop. (ii) The present market price is beneath equilibrium.

In the short run, no profit-oriented monopolistically-competitive firm still knowingly generates any output unless: (1) an economic profit is assured. (2) total revenues are expected to equal or exceed its total variable costs. (3) the average wage ra

Refer to the following diagrams give the answer of following question. In which case would the coefficient of income elasticity be positive? 1) A 2) B 3) C 4) D Q : Amount of output supplied and price The amount of output supplied is exactly proportional to the price therefore the price elasticity of supply equivalents one into: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Q : Demonstrates the Lorenz Curve This This given figure demonstrates as: (w) Lorenz curve. (x) familial income distribution graph. (y) Gini curve. (z) Blanc income standard curve. Q : Single monopoly in market A monopoly is A monopoly is a single: (w) seller of differentiated products. (x) producer of a good for that there are no close substitutes. (y) producer of a good for that there are several substitutes. (z) buyer of products into the market. Q : Example of a vertical merger An example An example of the vertical merger would be: (i) Merging the Oscar Myer hot dog Company with Wrangler Jeans Company and Aquafina Water Company. (ii) The log cabin architecture firm merging with the logging company and construction company. (iii) Merger between Wachovia

The amount of output supplied is exactly proportional to the price therefore the price elasticity of supply equivalents one into: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Q : Demonstrates the Lorenz Curve This This given figure demonstrates as: (w) Lorenz curve. (x) familial income distribution graph. (y) Gini curve. (z) Blanc income standard curve. Q : Single monopoly in market A monopoly is A monopoly is a single: (w) seller of differentiated products. (x) producer of a good for that there are no close substitutes. (y) producer of a good for that there are several substitutes. (z) buyer of products into the market. Q : Example of a vertical merger An example An example of the vertical merger would be: (i) Merging the Oscar Myer hot dog Company with Wrangler Jeans Company and Aquafina Water Company. (ii) The log cabin architecture firm merging with the logging company and construction company. (iii) Merger between Wachovia

This given figure demonstrates as: (w) Lorenz curve. (x) familial income distribution graph. (y) Gini curve. (z) Blanc income standard curve. Q : Single monopoly in market A monopoly is A monopoly is a single: (w) seller of differentiated products. (x) producer of a good for that there are no close substitutes. (y) producer of a good for that there are several substitutes. (z) buyer of products into the market. Q : Example of a vertical merger An example An example of the vertical merger would be: (i) Merging the Oscar Myer hot dog Company with Wrangler Jeans Company and Aquafina Water Company. (ii) The log cabin architecture firm merging with the logging company and construction company. (iii) Merger between Wachovia

A monopoly is a single: (w) seller of differentiated products. (x) producer of a good for that there are no close substitutes. (y) producer of a good for that there are several substitutes. (z) buyer of products into the market. Q : Example of a vertical merger An example An example of the vertical merger would be: (i) Merging the Oscar Myer hot dog Company with Wrangler Jeans Company and Aquafina Water Company. (ii) The log cabin architecture firm merging with the logging company and construction company. (iii) Merger between Wachovia

An example of the vertical merger would be: (i) Merging the Oscar Myer hot dog Company with Wrangler Jeans Company and Aquafina Water Company. (ii) The log cabin architecture firm merging with the logging company and construction company. (iii) Merger between Wachovia

When average production cost for Plastibristle Inc. falls like market demand increases and more firms go into the industry, Plastibristle is within: (1) an economically efficient industry. (2) a purely competiti

When point e corresponds to $18 per copy for St. Valentine’s Day software, so Prohibition Corporation can produce annual economic profit of at most just about: (i) $100 million. (ii) $140 million. (iii) $200 million. (iv) $300 million. (v) $400

18,76,764

1960599 Asked

3,689

Active Tutors

1412356

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!