Goods and services

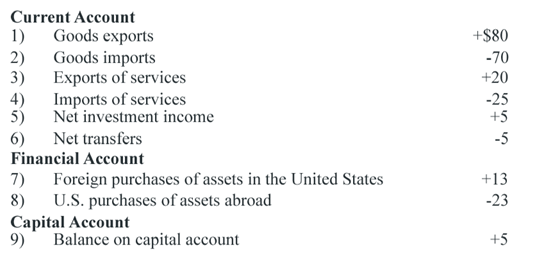

Refer to the above data. Choose the right answer from following. Zabella's balance on goods and services illustrates a: A) $5 billion deficit. B) $5 billion surplus. C) $10 billion surplus. D) $15 billion deficit.

pizza and sausage substitute or compliment wheat and rye substitute or compliment

I have a problem in economics on Competitive Markets-Labor unions. Please help me in the following question. The purely competitive labor markets are not characterized through: (1) Most of the individual buyers and sellers of the labor services. (2) S

The substitution effect helps most in describing why: (1) Demand curves slope down. (2) Goods are either complements or substitutes. (3) Air travel costs less than by walking the cross country. (4) Uncertainty regarding quality justifies govt. control

The assumption about buyers and sellers has good market information makes sure that they: (w) know everything. (x) never make errors. (y) can foretell the future. (z) won’t pay more than they have to, or sell for less than the market price.

I have problem in this question based on law of demand. Provide me correct answer of this. Described the circumstances in which the "general law of demand" not hold?

(a) Explain the relationship between full employment of resources and full production. (b) Look at the following production possibilities curve illustrating the possibilities in Sluggerville for producing bats and/or p

Relative to the resource demands from purely competitive sellers, demands through imperfectly competitive firms for resources tend to: (1) Perfectly price elastic. (2) Upward sloping. (3) Backward bending. (4) Less price elastic. (5) Perfectly price inelastic.

When a purely competitive firm functions in a competitive resource markets in short run then the firm: (i) Confronts an inelastic supply curve for the output. (ii) Purchases inputs till the net cost of inputs equivalents the net value of outputs. (iii

From around 1890 until 1970 year, the “structure-conduct-performance paradigm” dominated theories concerning how firms behave in various types of markets. Here the word “performance” in this context consider to things as: (i) d

For normal luxuries and goods, decreases in income tend to cause the: (i) Market prices to increase. (ii) Raises in quantities demanded. (iii) A reduction in demand for goods. (iv) Demand curves to shift to right. What is the right

18,76,764

1946436 Asked

3,689

Active Tutors

1423851

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!