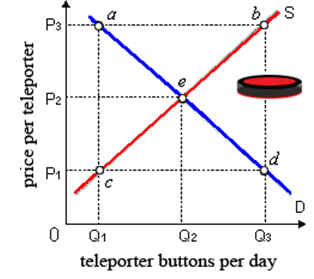

All prospective demanders [buyers] would be within equilibrium when this market for teleporter buttons created a price and a quantity consistent along with: (1) eliminating the shortage Q1-Q3 existing at P3. (2) any point along the demand curve within this market. (3) only price P2 and quantity Q2 at point a. (4) eliminating the surplus Q3-Q1 at price P1. (5) any point along the supply curve in this market.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?