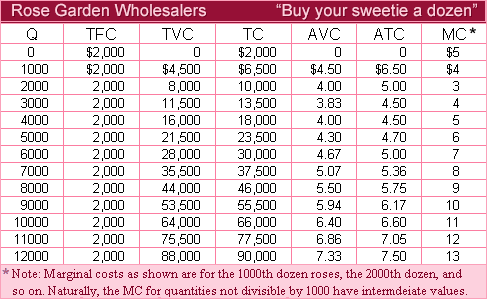

When the wholesale price P = $3 per dozen increased, this purely competitive increased farm maximizes profit with producing ___ dozen increased at a total (loss or profit) of $___. (i) zero; loss; $2000. (ii) 2000; loss; $1500. (iii) 3000; profit; $1500. (iv) 4000; profit; $4,500. (v) 4000; profit;$2,000.

Can someone explain/help me with best solution about problem of Economics...