Elucidate Production Possibility curve with the help of a diagram?

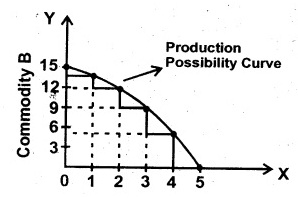

Answer: The Production Possibility Curve refers to a curve that shows various production possibilities which can be produced with specified resources and technology.

When the economy devotes all its resources to the production of commodity B, it can generate 15 units however then the production of commodity A will be zero. There can be much production possibilities of commodity A & B. When we want to generate more commodities B, we have to decrease the output of commodity A and vice-versa.