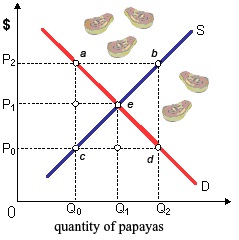

The excess of papayas would appear when: (1) seller’s supply prices increase to P1. (2) Govt. set a price ceiling of P1. (3) Growers predicted prices to soar. (4) Hurricane destroyed all Central American papaya plantations. (5) Government obliged a price floor of P2.

Please someone suggest me the right answer.