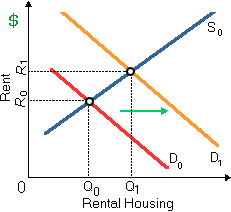

After the change within the demand curve for housing as: (1) a temporary housing shortage may exist at R0. (2) landlords will have more complexity repaying their mortgages. (3) rental rates will fall below interest payments. (4) equilibrium prices for houses will reduce. (5) a surplus of housing exists at R1.

I need a good answer on the topic of Economic problems. Please give me your suggestion for the same by using above options.