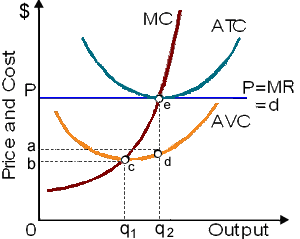

Estimate total fixed costs for profit-maximizing firm

Total fixed costs for such profit-maximizing firm equivalent: (1) 0bcq1. (2) 0adq2. (3) 0Peq2. (4) aPed. (5) Can't be measured in illustrated figure. Can anybody suggest me the proper explanation for given problem regarding Economics generally?

Total fixed costs for such profit-maximizing firm equivalent: (1) 0bcq1. (2) 0adq2. (3) 0Peq2. (4) aPed. (5) Can't be measured in illustrated figure.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?

The word ‘double taxation’ signifies to: (i) The Corporation paying both the federal and state taxes. (ii) Corporations paying the corporate income tax and shareholders paying the personal income tax on dividends. (iii) Both partners in pa

Can someone help me in finding out the right answer from the given options. According to the law of diminishing marginal utility, the longer that Chris and Lee kiss: (i) The less invested each will be in enduring this relationship. (ii) The closer they are to arriving

Increasing the price of a product will raise total revenue proportionally into the unlikely event which demand was: (1) perfectly price elastic. (2) relatively price elastic. (3) unitarily price elastic. (4) relatively price inelastic (5) perfectly price inelastic.

Question: (a) Suppose the income elasticity of demand for pre-recorded music compact disks is +4 and the income elasticity of demand for a cabinet maker's work is +0.4. Compare the impact on pre-recorde

Negative income tax programs attack poverty through: (w) levying heavy taxes on the poor to encourage them to work more. (x) providing transfers in kind to low income households. (y) providing cash subsidies to guarantee a minimum income to low income

The official “poverty line” computed by the federal government is the income level needed to meet the perceived fundamental needs of families along with differing characteristics as size, location, etc. Therefore, it is based on: (1) a rel

Describe the relationship among Average Variable Cost (AVC) Average, Total Cost (ATC) and marginal Cost (MC)? Answer: A) If MC

When the interest rate is 5 percent and a financial investment produces annual payments of $50,000, in that case the present value of this asset is as: (w) $1,000,000. (x) $5,000,000. (y) $500,000. (z) $10,000,000.

Find out the price elasticity of supply at any point on a straight line curve when A) supply curve intersects ox axis in its negative range B) supply curve intersects ox axis in its positive range. C) Supply curve passes via the origin?

Unlike a monopolistically competitive firm, which an oligopoly is described by: (w) product differentiation. (x) extensive use of advertising. (y) conscious interdependence in decisionmaking by firms. (z) independence among firms. Discover Q & A Leading Solution Library Avail More Than 1427210 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1927638 Asked 3,689 Active Tutors 1427210 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1927638 Asked

3,689

Active Tutors

1427210

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!