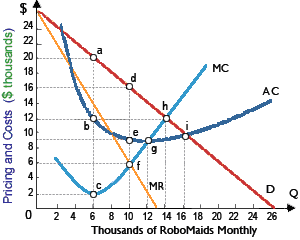

Estimate profit-maximizing price

The profit-maximizing price for RoboMaids is: (1) $24,000 per robot. (2) $20,000 per robot. (3) $16,000 per robot. (4) $12,000 per robot. (5) $10,000 per robot. Can someone explain/help me with best solution about problem of Economics...

The profit-maximizing price for RoboMaids is: (1) $24,000 per robot. (2) $20,000 per robot. (3) $16,000 per robot. (4) $12,000 per robot. (5) $10,000 per robot.

Can someone explain/help me with best solution about problem of Economics...

When this firm initially had important market power along with potential long-run economic profit, a likely cause of the firm finally being in a stable equilibrium of an $18 price and output of 5,000 units every day would be: (1

I have a problem in economics on Power of monopsonist. Please help me in the given question. The firm which is the sole buyer of a specific good or resource is a: (i) Monopsonist. (ii) Plutocracy. (iii) Bilateral monopolist. (iv) Price discriminator.

An oligopoly will maximize profits when this produces where: (w) MR > MC. (x) MR = MC. (y) TR = TC. (z) MR > P. Can anybody suggest me the proper explanation for given problem regarding Economics

If a monopolist’s marginal revenue is zero, then: (1) total revenue is zero. (2) demand is perfectly inelastic. (3) the price of the product exceeds average cost. (4) economic profit is zero. (5) total revenue is maximized. Q : Monopolistic Exploitation-Demand for I have a problem in economics on Monopolistic Exploitation-Demand for Labor. Please help me in the following question. The monopolistic exploitation is exercised if the employment equilibrium for a firm involves: (i) MRP > MFC. (ii) Paying the work

I have a problem in economics on Monopolistic Exploitation-Demand for Labor. Please help me in the following question. The monopolistic exploitation is exercised if the employment equilibrium for a firm involves: (i) MRP > MFC. (ii) Paying the work

Provide the solution of this question. The problem of asymmetric information is that: A) neither health care buyers nor providers are well-informed. B) health care providers are well-informed, but buyers are not. C) the outcomes of many complex medical procedures cannot be predicted. D) insurance co

Even though the concentration ratio for an oligopoly is close to hundred, firms may operate rather efficiently when the market: (1) price conforms to a limit pricing model. (2) is contestable since entry and exit are easy. (3) demand curve is unitaril

Extensive national advertising can be a form of: (1) natural barrier. (2) strategic barrier. (3) regulatory barrier. (4) price discrimination. (5) moral hazard. Can anybody suggest me the proper explanation for given problem regard

When a price hike for Big Gulps of GlugaChug from $1 to $2 improves sales of dehydrated water from 50 to 100 kegs, then the dehydrated water and GlugaChug are: (1) Joint outputs in the production. (2) Complements. (3) Substitutes. (4) Mixed resource alternatives.

The quantity dinner salads demanded is 100 everyday while Café Les Gourmands charges a price of $1.80, although when price drops by $1, quantity demanded is one hundred fifty. The price elasticity of demand for dinner salads at such restaurant

18,76,764

1951126 Asked

3,689

Active Tutors

1439040

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!