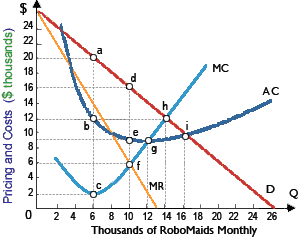

Robomatic Corporation could attain minimum average costs for RoboMaids when this produced: (1) 4,000 robots per month. (2) 6,000 robots per month. (3) 8,000 robots per month. (4) 10,000 robots per month. (5) 12,000 robots per month.

Hey friends please give your opinion for the problem of Economics that is given above.