Equilibrium price in the short run

The equilibrium price for Christmas trees in the short run is: (w) P1. (x) P2. (y) P3. (z) P4. How can I solve my Economics problem? Please suggest me the correct answer.

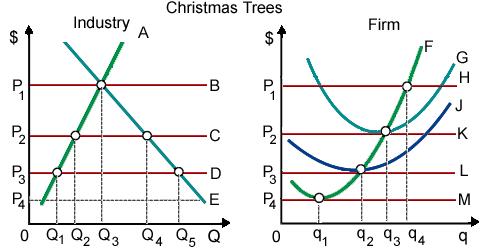

The equilibrium price for Christmas trees in the short run is: (w) P1. (x) P2. (y) P3. (z) P4.

How can I solve my Economics problem? Please suggest me the correct answer.

Both demand and supply of hamburgers would plummet in short run, as would be quantity sold, however we can’t be certain how the price would adjust when: (i) 75 % of the population became serious vegetarians. (ii) People abruptly decreased their intake of milk pr

I have a problem in economics on Short Run-input of firms cannot be changed. Please help me in the following question. In short run, the firm: (i) Can change any input. (ii) Can’t change any input. (iii) Cannot change the output. (iv) Has at lea

Pure competitors in a long-run equilibrium are paid a price which: (i) allows recovery of any previous operating losses. (ii) equals MC although exceeds average cost. (iii) maximizes average revenue minus average cost. (iv) equals maximum long run ave

I have a problem in economics on Hike in relative price of a good. Please help me in the following question. The hike in relative price of a good will quickly increase the: (i) Quantity demanded. (ii) Market supply. (iii) Rate of inflation. (iv) Quant

Can someone help me in finding out the right answer from the given options. Both level of employment through a firm and the average rate of monopsonistic exploitation of labor are raised when a firm is capable to: (1) Outsource through hiring less productive workers i

The arc elasticity of demand of Ajax for labor in between point b and point c is approximately: (1) 0.30. (2) 0.60. (3) 0.90. (4) one. (5) two. Q : Is cotton textile is macroeconomic or Is the study of cotton textile business a macroeconomic or a microeconomic study? Answer: The study of cotton textile business is a microeconomic study.

Is the study of cotton textile business a macroeconomic or a microeconomic study? Answer: The study of cotton textile business is a microeconomic study.

Opinion of Frank Knight, about economic profits is: (1) rewards for bearing uncertainty. (2) easily capitalized for firms possessing monopoly power. (3) rewards for innovation. (4) easily predicted when competent economic forecasting is employed. (5) equal to accounti

Can someone please help me in finding out the most accurate answer from the following question. The Economic profit equivalents: (1) Accounting profit minus the implicit costs. (2) Normal profit. (3) Net revenue minus the implicit costs. (4) Net revenue minus the expl

Economically, the labor unions can be thought of as the: (i) encouraging competition between the workers for jobs. (ii) Rising the flexibility of nominal wages. (iii) Attempts to cartelize and unite the individual sellers of labor. (iv) Having a goal of the minimum un

18,76,764

1941355 Asked

3,689

Active Tutors

1452157

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!