Equilibrium price in short run

The equilibrium prices for cranberries within the short run of: (w) P1. (x) P2. (y) P3. (z) P4. I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.

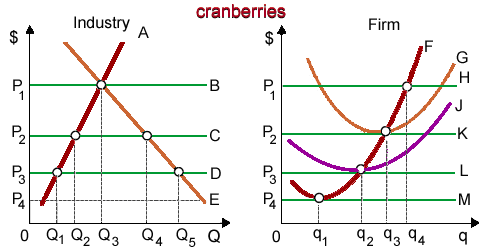

The equilibrium prices for cranberries within the short run of: (w) P1. (x) P2. (y) P3. (z) P4.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.

When curve C reflects the long run supply curve as in demonstrated figure for this industry, in that case this is a/an: (w) decreasing cost industry. (x) increasing cost industry. (y) constant cost industry. (z) diseconomies of scale industry.

The market demands for automobiles are not rapidly and directly influenced by modifications in: (i) Income. (ii) Gasoline prices. (iii) Salaries paid to auto-workers. (iv) The number of legal drivers. (v) Preferences and tastes. Q : CAPM and Portfolio The information is The information is illustrated below: (a) Determine the expected return on Stock X?

The information is illustrated below: (a) Determine the expected return on Stock X?

An asset’s associate “liquidity” is inversely measured through the: (w) transaction costs in dealing within the asset as a proportion of the market price of the asset. (x) time it takes to convert this to cash. (y) “backing&rdq

Market demand curve: The market demand also rises with a fall in price and vice-versa. In figure below the quantity demanded by

When diet faddists gulp 205 million unsweetened as “No-Carb” milkshakes of $2.30 apiece, if cut back to 155 million per week while the price rises to $3.70 every, the price elasticity of their demand for shakes equivalents

Since lifetime earning patterns differ, in that case the Gini index will: (1) continue to rise over time. (2) never reach zero or perfect equality. (3) remain constant. (4) surpass 100 in the near future. (5) be lower for developing countries than for

Why the Okun's Law Coefficient Is so Large? Okun's Law posits not a 1-to-1 relation but a 2.5-to-1 relationship between real GDP growth and the unemployment rate. That is, a one percentage-point fall in the unemployment rate is associated not with a 1 but a 2.5 percent boost in the level of produ

When this firm cannot price discriminate, after that the rate of economic inefficiency per unit of output which its exercise of market power yields equals to: (i) area 0PbQ0. (ii) distance af. (iii) area 0fcQ0. (iv) distance bc. (v) r

The raise in the supply of potatoes is probable to decrease the: (i) Supply of potato harvesters. (ii) Demand for pasta and rice. (iii) Price of Big Macs. (iv) Quantity of ketchup people put on hot-dogs. (e) Budgets of most house-holds.

18,76,764

1922877 Asked

3,689

Active Tutors

1454512

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!