Effect of an increase in the price

Which of the following diagrams depictes(s) the effect of an increase in the price of Budweiser beer on the market for Coors beer? A) A and C. B) A only. C) B only. D) C only. Give me the answer of above question

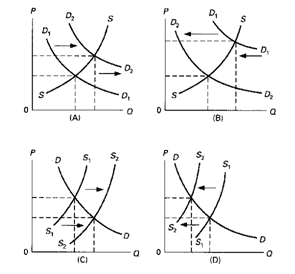

Which of the following diagrams depictes(s) the effect of an increase in the price of Budweiser beer on the market for Coors beer? A) A and C. B) A only. C) B only. D) C only.

Give me the answer of above question

When the present value of the expected future income by additional investment exceeds the current cost of additional investment, in that case investment will: (w) rise. (x) fall. (y) not change. (z) There is insuffici

On such demand curve, the demand for DVD games is completely elastic at a price of: (w) $50. (x) $25. (y) $20. (z) None of the above. Q : Pay annual income by perpetuities bonds When all bonds are perpetuities which pay annual income of $50, at an interest rate of 5% the price of bonds is: (w) $1,000. (x) $500. (y) $100. (z) $750. Can someone explain/help

When all bonds are perpetuities which pay annual income of $50, at an interest rate of 5% the price of bonds is: (w) $1,000. (x) $500. (y) $100. (z) $750. Can someone explain/help

I have a problem in economics on spending pattern in Substitution Effects. Please help me in the following question. Even when your real income were held steady by adjusting for price modifications, your spending pattern would react to modifications in relative prices

At the point on the demand curve for RoboMaids where the price elasticity of demand is unitary, the price would be roughly: (i) $10,000, resulting in sales of roughly 16,000 robots monthly. (ii) $13,000, resulting in sales of approxim

I am facing problem in this question. Help me in find out correct answer of this economic based question. Explain interdependent economy? Illustrate it by using an input-output table and model.

Whenever the market for the good is in equilibrium, this signifies that the: (i) Demand and supply are equivalent. (ii) Tax wedge is perfectly offset by the government advantages. (iii) Differences among demand prices and supply prices equivalent profit per unit. (iv)

Describe the Reallocation of resources objective of the government budget.

For a purely competitive market at any equilibrium point on the short-run supply curve: (w) all firms have identical marginal costs. (x) economic profit is positive. (y) accounting profit is normal. (z) marginal revenue = average cost. Q : Price discriminate A monopolist selling A monopolist selling several di erent products can sometimes "price discriminate" by bundling her products together. Here's an example. Suppose the U of C is planning to o er a series of two concerts. The rst program in the series consists of music by Chopin; the second, music by Stravinsky

A monopolist selling several di erent products can sometimes "price discriminate" by bundling her products together. Here's an example. Suppose the U of C is planning to o er a series of two concerts. The rst program in the series consists of music by Chopin; the second, music by Stravinsky

18,76,764

1959187 Asked

3,689

Active Tutors

1455636

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!