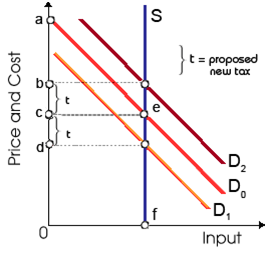

When D0 is the initial demand curve for land in this illustrated figure, within equilibrium the economic rent realized through the landowner will be: (1) zero. (2) area Ocef. (3) area cae. (4) area Oaef. (5) a pure economic profit.

Please guys help to solve this problem of Economics with some explanation.