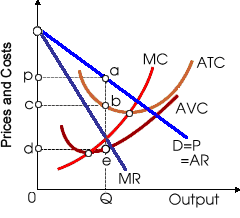

When this monopolistic competitor produces Q units, this is maximizing: (w) sales development and its market share. (x) total revenue. (y) economic profits. (z) total fixed cost and its managers' salaries.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?