Economic profits in the long run

In this illustrated figure in below the firm probably to have economic profits in the long run would be as: (w) Firm A. (x) Firm B. (y) Firm C. (z) Firm D. How can I solve my Economics problem? Please suggest me the correct answer.

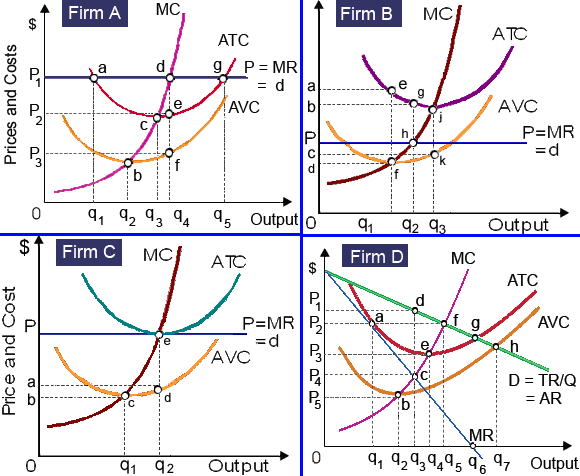

In this illustrated figure in below the firm probably to have economic profits in the long run would be as: (w) Firm A. (x) Firm B. (y) Firm C. (z) Firm D.

How can I solve my Economics problem? Please suggest me the correct answer.

Can someone help me in finding out the right answer from the given options. Zeus got one million dollars for winning every event in current Olympics. In past, he would have frivolously exhausted his winnings on the lightning bolts, however after studying economics, he

The price elasticity of supply as in below demonstrated figure is unitary within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Q : Nominal Interest Rates Nominal interest Nominal interest rates are: (w) always identical to real interest rates. (x) the percentage of monetary premiums paid per time era for the use of money. (y) determined by the size of economic rents. (z) the percentage of purchasing power transferred b

Nominal interest rates are: (w) always identical to real interest rates. (x) the percentage of monetary premiums paid per time era for the use of money. (y) determined by the size of economic rents. (z) the percentage of purchasing power transferred b

Explain the term PHP?

I have a problem in economics on Bilateral Monopoly problem. Please help me in the following question. The bilateral monopoly is in operation when: (1) The firm is mere employer of some labor force and a union is the mere supplier of the labor for tha

When governments compelled pharmaceutical producers to manufacture and sell at least Q3 penicillin, in that case the: (1) purely-competitive firms which produced penicillin would experience persistent economic profits. (2) resulting inadequate antibiotic tr

Perfectly equal distributions of income or wealth are reflected within the Lorenz curve demonstrated as: (i) line 0A0'. (ii) line 0B0'. (iii) line 0C0'. (iv) line 0D0'. (v) line 0E0'. Q : Problem on market boundaries The The market’s boundaries are stated by: (i) Legislation. (ii) The number of sellers and buyers in the market. (iii) The ease of trading among sellers and buyers. (iv) Geographical borders. Choose the right ans

The market’s boundaries are stated by: (i) Legislation. (ii) The number of sellers and buyers in the market. (iii) The ease of trading among sellers and buyers. (iv) Geographical borders. Choose the right ans

The supply curve for perishable goods which, once produced, can’t be stored in inventory is generally functioned as perfectly price inelastic into the: (i) short-run. (ii) intermediate period. (iii) long-run. (iv) market period. (v) fiscal year

By 2000, the differential among the rich and the poor which can be attributed to economic discrimination was computed at: (w) approximately 60 percent. (x) approximately 30 percent. (y) under 10 percent. (z) zero.

18,76,764

1961065 Asked

3,689

Active Tutors

1459098

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!