Economic profit generating purely competitive firm

In this illustrated figure in below the only purely competitive firm currently generating economic profit is in: (w) Firm A. (x) Firm B. (y) Firm C. (z) Firm D. Hello guys I want your advice. Please recommend some views for above Economics problems.

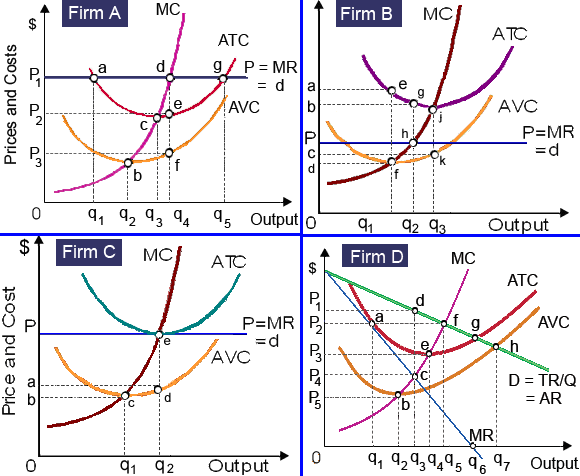

In this illustrated figure in below the only purely competitive firm currently generating economic profit is in: (w) Firm A. (x) Firm B. (y) Firm C. (z) Firm D.

Hello guys I want your advice. Please recommend some views for above Economics problems.

Technological advances have raised agricultural productivity enormously among 1800 and nowadays, and therefore, the relative incomes of family farmers declined dramatically. There hardships endured through American farm families throughout this period

When the nominal price of apples at a remote orchard is fewer than at a local grocery store, in that case you are more probable to buy at the orchard when: (w) at all possible, because produce is invariably cheaper at the orchard. (x) you desire to bu

Why Vietnam divided into two different nations?

The _______ price for a lately issued bond signifies that the firm issuing the bond is paying the _______ interest rate to borrow the funds. (1) Lower; lower. (2) Lower; higher. (3) Higher; higher. (4) None of the above. The interest rate is fixed. Q : Ownership shares in corporation I have I have a problem in economics on Ownership shares in corporation. Please help me in the following question. The Ownership shares in a corporation are termed as: (1) Bonds. (2) Entrepreneurial capital. (3) Common stock. (4) Total worth. (5) Retained equity.

I have a problem in economics on Ownership shares in corporation. Please help me in the following question. The Ownership shares in a corporation are termed as: (1) Bonds. (2) Entrepreneurial capital. (3) Common stock. (4) Total worth. (5) Retained equity.

I have a problem in economics on Area above price line and below individual demand curve. Please help me in the following question. When a single price is charged for each and every unit of a good, then the area above the price line however beneath an individual&rsquo

You win the Idaho state lottery as well as are entitled to two tax-free payments of $500,000 every. You get the first payment today and the next payment in precisely one year. Suppose the interest rate is a generally high 25 percent.

Can someone please help me in finding out the accurate answer from the following question. As compared to men with identical amounts of experience or education, women on an average earn: (1) Higher wages. (2) Similar wages. (3) Lower wages. (4) There is no special pat

When an individual or family lacks adequate resources to escape a state of destitution, their circumstances are described as: (1) involuntary poverty. (2) relative poverty. (3) a vicious cycle of poverty (4) institutional poverty. (5) a culture of pov

Hey FRIEND I need your help for query as given below: The price elasticity beside a horizontal demand curve is constant at: (w) zero. (x) infinity. (y) 1. (z) -1. Can someone ex

18,76,764

1935640 Asked

3,689

Active Tutors

1449338

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!