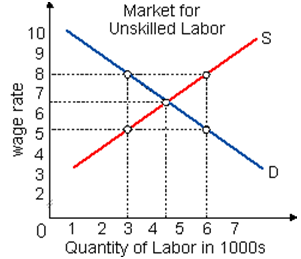

A minimum legal wage of $5 per hour in this market for unskilled labor would: (w) have no effect on employment or the wages paid. (x) create new jobs for 3,000 unskilled workers. (y) move some low-skilled workers above the poverty line. (z) create unemployment for 3,000 unskilled workers.

I need a good answer on the topic of Economic problems. Please give me your suggestion for the same by using above options.