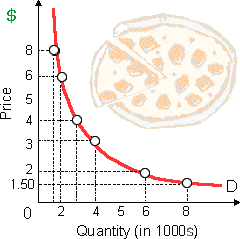

Assume that many students have fixed “pizza budgets.” When the price per slice falls by $10 to $1 along such demand curve for pizza weekly near a college campus, then the price elasticity of demand for pizza: (w) rises towards infinity. (x) falls towards zero. (y) rises, then falls. (z) always equals 1 and demand is unitarily elastic.

Hello guys I want your advice. Please recommend some views for above economics problems.