Determine total variable cost of a firm

This firm’s total variable cost (TVC) equals area as: (w) 0phq2. (x) daef. (y) 0bgq2 minus area daef. (z) obgq2. I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.

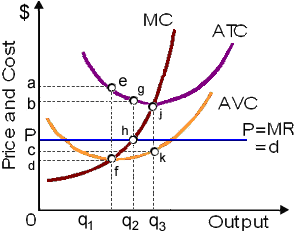

This firm’s total variable cost (TVC) equals area as: (w) 0phq2. (x) daef. (y) 0bgq2 minus area daef. (z) obgq2.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.

The social goal of providing the biggest happiness to the most people is intent to practice the: (i) Precautionary discretion. (ii) Classical theory. (iii) Utilitarianism. (iv) Speculative balances. (v) Arbitrage. Can someone pleas

When a firm shuts down within the short run, in that case it’s economic: (w) profit is zero. (x) resources have zero opportunity cost. (y) loss equals its fixed cost. (z) value to shareholders rises. Please guys help to solve

Rent controls set under equilibrium tend to cause: (w) simpler access to affordable housing. (x) apartment construction to boom. (y) the quantity and upkeep of rental units to fall. (z) less racial discrimination within housing. Q : Company Unions-tools for managers Can Can someone please help me in finding out the accurate answer from the following question. Unions which act primarily as the tools for managers of a firm are termed as: (1) Managerial unions. (2) Company unions. (3) Wildcat unions. (4) Union-busters.

Can someone please help me in finding out the accurate answer from the following question. Unions which act primarily as the tools for managers of a firm are termed as: (1) Managerial unions. (2) Company unions. (3) Wildcat unions. (4) Union-busters.

Describe how changes in the prices of other products influence the supply of a specific product.

For water the price elasticity of demand is: (w) low since the price is high. (x) high since the price is high. (y) high since there are few substitutes for water. (z) low since this has few substitutes and a low price. Q : Price elasticity of demand I have a I have a problem related to price elasticity of demand. The question is illustrated as "After the price of movie tickets rose, I spent less money on movie tickets." What can you infer regarding my price elasticity of demand?

I have a problem related to price elasticity of demand. The question is illustrated as "After the price of movie tickets rose, I spent less money on movie tickets." What can you infer regarding my price elasticity of demand?

Can someone help me in finding out the right answer from the given options. According to the law of diminishing marginal utility, the longer that Chris and Lee kiss: (i) The less invested each will be in enduring this relationship. (ii) The closer they are to arriving

Maggie thinks there are main differences among Crest, Colgate, Aquafresh and Rembrandt toothpastes, and eventually chooses Crest. Therefore her perception is mainly a consequence of: (1) successful product differentiation. (2) monopolistic competition. (3) informative

Predatory behavior would not comprise: (w) lowering prices. (x) expanding output. (y) rapid technological innovation. (z) raising prices. Can anybody suggest me the proper explanation for given problem regarding

18,76,764

1948924 Asked

3,689

Active Tutors

1419469

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!