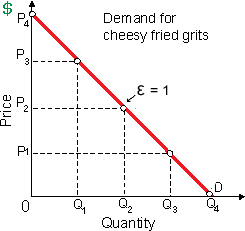

As the price falls by P4 to P3 to P2 to P1 beside such demand curve for Pixie's cheesy fried grits, then total revenue: (w) always rises. (x) always falls. (y) rises then falls. (z) falls then rises.

How can I solve my Economics problem? Please suggest me the correct answer.