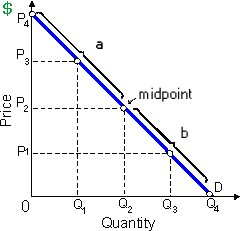

In this demonstrated figure, the total revenue: (w) varies inversely along with price in range b. (x) is minimized at the midpoint of the demand curve. (y) remains unchanged like price changes within range b. (z) will raise as price falls within range a.

How can I solve my Economics problem? Please suggest me the correct answer.