Determine total fixed cost

This profit-maximizing pure competitor’s fixed cost (TFC) can be calculated as area of: (1) 0Phq2. (2) 0bgq2. (3) Pbgh. (4) 0aeq1. (5) daef. Hello guys I want your advice. Please recommend some views for above Economics problems.

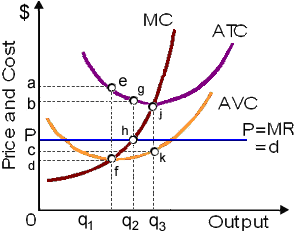

This profit-maximizing pure competitor’s fixed cost (TFC) can be calculated as area of: (1) 0Phq2. (2) 0bgq2. (3) Pbgh. (4) 0aeq1. (5) daef.

Hello guys I want your advice. Please recommend some views for above Economics problems.

When the last unit produced and sold adds $100 to revenue of a firm and $75 to its costs, this will: (a) increase output to increase profit. (b) reduce output to increase profit. (c) maintain similar level of output to maximize profit. (d) shut down. Q : Tax cutting affect the economy How does How does tax cuts affect the economy?

How does tax cuts affect the economy?

Can someone please help me in finding out the accurate answer from the following question. When implicit cost surpasses implicit revenue and economic profit is zero (0), then accounting profit is: (1) Bigger than zero. (2) Zero. (3) Less than 0 (zero). (4) Not specifi

Whenever your purchasing power drops as the price of a good you purchase increases, you make adjustments as of the: (1) Marginal utility effect. (2) Price level effect. (3) Income effect. (4) Consumer excess effect. Choose the righ

Question: (a) Suppose the income elasticity of demand for pre-recorded music compact disks is +4 and the income elasticity of demand for a cabinet maker's work is +0.4. Compare the impact on pre-recorde

The phrase ‘dollar votes’ refers to the consumers: (1) Voting patterns in the national elections. (2) Recognizing what goods are produced. (3) Each containing an equivalent says about what is generated. (4) Being subservient to big firms. Q : Total variable cost while maximizes Total cost when such firm maximizes economic profits would be: (w) $72,000 per period. (x) $80,000 per period. (y) $96,000 per period. (z) $100,000 per period. Q : Labor-Leisure Tradeoffs When leisure is When leisure is a normal good, then the demand for leisure: (i) Differs directly with the income. (ii) Has declined sharply as World War II. (iii) Is positively associated to the average age of population. (iii) Shifts left-ward as an outcome of technological advances

Total cost when such firm maximizes economic profits would be: (w) $72,000 per period. (x) $80,000 per period. (y) $96,000 per period. (z) $100,000 per period. Q : Labor-Leisure Tradeoffs When leisure is When leisure is a normal good, then the demand for leisure: (i) Differs directly with the income. (ii) Has declined sharply as World War II. (iii) Is positively associated to the average age of population. (iii) Shifts left-ward as an outcome of technological advances

When leisure is a normal good, then the demand for leisure: (i) Differs directly with the income. (ii) Has declined sharply as World War II. (iii) Is positively associated to the average age of population. (iii) Shifts left-ward as an outcome of technological advances

The Minimum wage legislation is UNLIKELY to aid: (i) Skillful workers who compete with untrained workers. (ii) Untrained workers who don’t lose their jobs. (iii) Buyers of goods which are more capital intensive associative to the buyers of labor intensive goods.

Opinion of Frank Knight, about economic profits is: (1) rewards for bearing uncertainty. (2) easily capitalized for firms possessing monopoly power. (3) rewards for innovation. (4) easily predicted when competent economic forecasting is employed. (5) equal to accounti

18,76,764

1955042 Asked

3,689

Active Tutors

1412381

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!