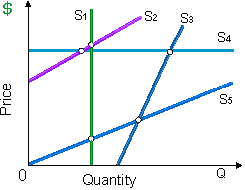

Assume that all such curves in below demonstrated graph are infinitely long straight lines. The supply curve which is perfectly price-elastic is: (1) supply curve S1. (2) supply curve S2. (3) supply curve S3. (4) supply curve S4. (5) supply curve S5.

Hello guys I want your advice. Please recommend some views for above Economics problems.