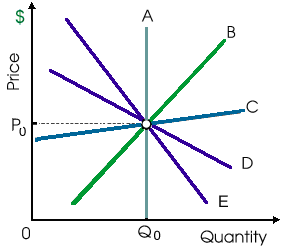

When curve C reflects the long run supply curve for this industry as in illustrated figure, in that case the short-run supply curve would be: (i) curve A. (ii) curve B. (iii) curve C. (iv) curve D. (v) curve E.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.