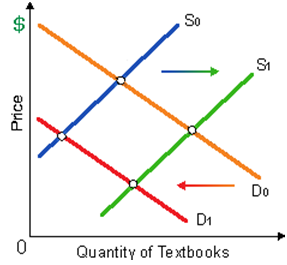

In this market for textbooks, demand has transferred from D0 to D1 and supply varied from S0 to S1. Such market for textbooks has experienced as: (w) a raise in demand and supply. (x) a reduce in demand and supply. (y) a raise in supply and a reduce in demand. (z) a raise in demand and a reduce in supply.

How can I solve my economics problem? Please suggest me the correct answer.