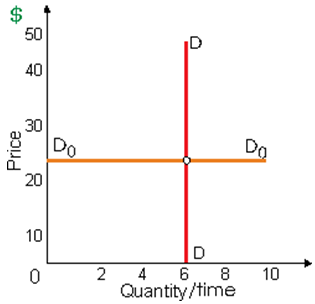

In below this demonstrated figure, there demand curve: (w) D0D0 is perfectly price-inelastic. (x) DD is perfectly price-elastic. (y) DD has a price elasticity coefficient of unity (1). (z) D0D0 has a price elasticity coefficient of infinity.

Please choose the right answer from above...I want your suggestion for the same.