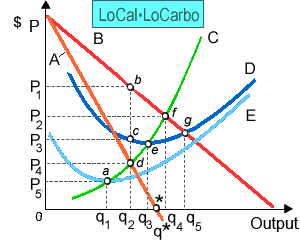

LoCalLoCarbo that is the favorite corporation of fad dieters maximizes profit by making: (1) output q1 . (2) output q2 . (3) output q3 . (4) output q4 . (5) output q5 .

Hey friends please give your opinion for the problem of Economics that is given above.