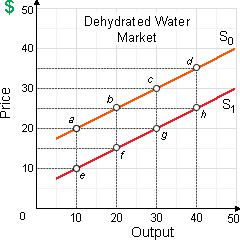

Of all of the known ranges on such supply curves, the supply of tanks of dehydrated water is least price elastic in between: (i) point a and point b. (ii) point b and point c. (iii) point c and point d. (iv) point e and point f. (v) point g and point h.

Please choose the right answer from above...I want your suggestion for the same.